Are you considering buying a house in Florida? If so, our Florida mortgage calculator will help you know how much house you can afford. This popular state has a lot to offer, so use the following information to your advantage.

Here’s what you need to know.

Mortgage Calculator for Florida

You can prepare for a mortgage in Florida with our free Florida mortgage calculator. You can use this same calculator for any state if you enter state-specific info. Here’s how the calculator works.

Our mortgage calculator uses a standard mathematical formula to calculate your monthly mortgage payments. Here’s the exact formula with a definition for each variable:

M = P[r(1 + r)^n / ((1 + r)^n) - 1)]

P = The principal loan amount. This is the money you borrow to buy the house. Say you buy a $400,000 house, put down $80,000, and take out a mortgage for the rest. The $320,000 you take out is your principal.

r = Your monthly interest rate. Your interest rate from your lender is an annual rate. Divide this by 12 to get your monthly rate. If your interest rate is 6.5%, divide that by 12 to get a monthly rate of 0.54%. Note that APR is different from interest rate. APR is also expressed as a percentage, but includes the fees we’ll discuss later in this article.

n = Total number of loan payments. This is your loan term multiplied by 12. So, if you have a 30-year mortgage, that’s 360 loan payments.

M = Your monthly mortgage payment. This is the total principal and interest you’ll pay every month.

With all the math explained, you should know there are other parts to consider. You see, in the real world, your monthly mortgage payment isn’t just principal and interest. It also includes property taxes and insurance. Additionally, you may have other housing costs outside of your mortgage payment, such as regular HOA fees. You’ll need to consider all of these for a correct estimate of how much housing in Florida will cost you.

Learn more about these costs below.

Average Closing Cost in Florida

The average closing costs for buyers in Florida is 2% to 5% of the home sale price. These costs include fees for title insurance, document preparation and filing, and lender fees for loan origination. That means if you buy a $400,000 house, closing costs will be $8,000 to $20,000 on average.

You won’t need to hire a real estate attorney in Florida to close on your house, but it’s recommended. If you do hire a lawyer to help you with the closing, you’ll also need to pay attorney fees.

Other Costs to Consider

Besides closing costs, principal, and interest, there are other costs that come with buying a home in Florida. By accounting for these in our mortgage calculator for Florida, you can get a more accurate estimate of your monthly payment.

Calculate Your Taxes

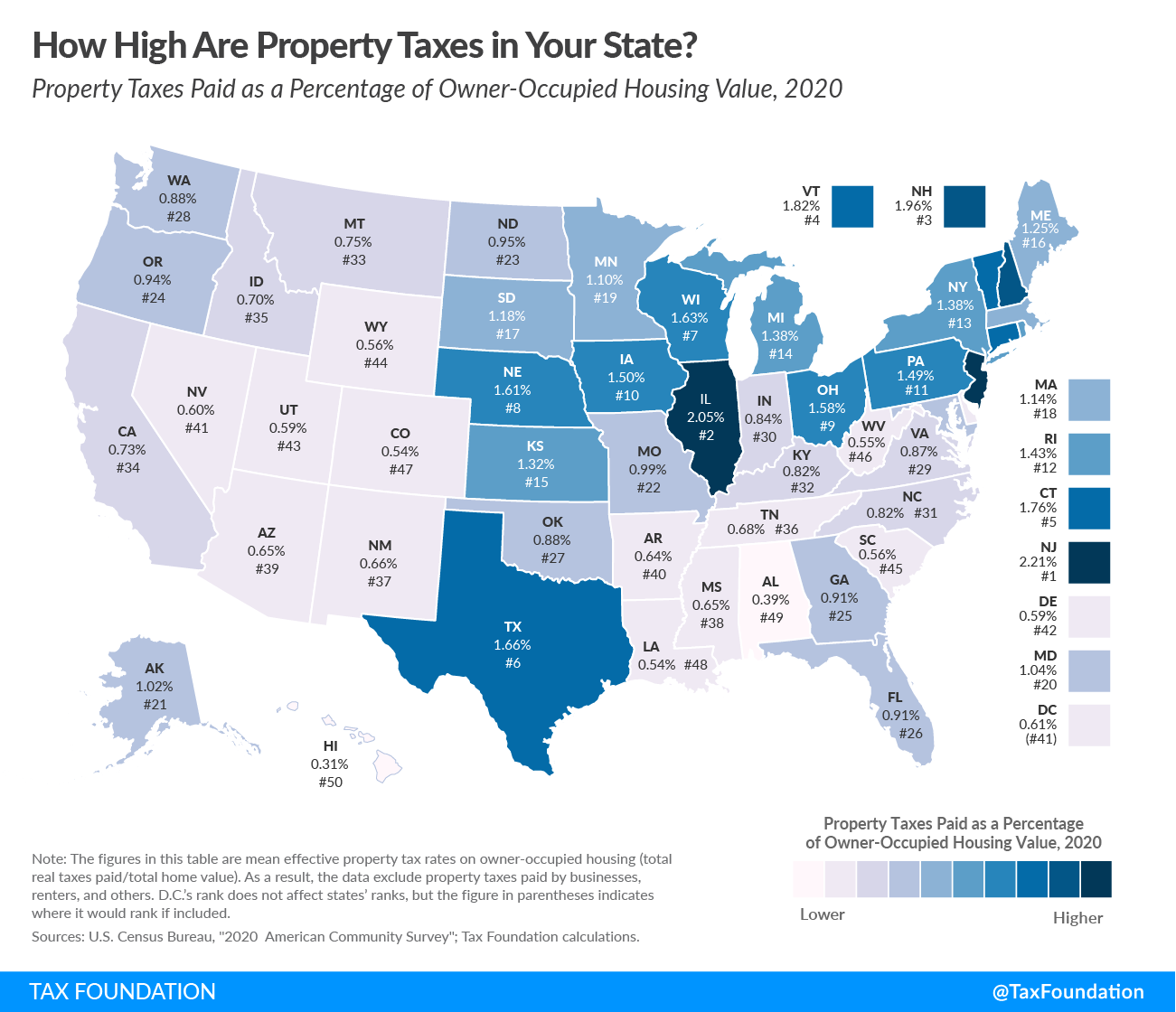

On the bright side, Florida doesn’t have high average property taxes. The state averages an effective property tax of 0.91%. Keep in mind that this can vary by county. For a $400,000 house, that effective rate translates to $3,640. However, research each county’s tax average before you buy in the area. If you already have a sale agreement on a house, you can also ask the seller for past property tax info to get a good idea of what to expect.

Certain jurisdictions sometimes have other tax abatement / adjustment programs that can impact your tax rate. Exemptions for primary residences are very common in vacation areas, for example, to levy a higher tax on properties used as a secondary residence. Once you know where you’re planning to buy a house, put some time into researching property tax rates in the area.

You can find your property tax rate in Florida by county here.

Insurance Coverage

Florida consistently ranks as one of the most expensive states for home insurance coverage. The state’s average homeowners insurance is $4,231 annually, which is almost three times the national average. That equates to $352.58 every month. You can use this average in our mortgage calculator for Florida. But keep in mind that this number fluctuates based on the value of the home, the location of the property, and the amount of coverage you have. (It’s fairly easy to get a ballpark quote from most insurance companies online.)

Unfortunately, one of the reasons Florida has such high homeowners insurance is the large amount of lawsuits insurance companies face there. This has caused many insurance companies to go bankrupt or withdraw from the Sunshine State.

There are also areas where some companies are hesitant to insure homes due to dangerous weather. So, you may see elevated rates in these areas as they’re riskier for providers and there isn’t a lot of competition.

Private Mortgage Insurance (PMI)

PMI is an additional fee lenders add to conventional loans if you put down less than 20% of the home price. PMI can vary between lenders, as widely as 0.1% to 2% of your loan amount annually. Your credit score and the size of your loan also play into how much you’ll pay for PMI. That means you need to ask your lender how much PMI would cost.

If you have a $400,000 mortgage, that’s a range of $400 to $8,000. So, if one lender charges 0.3% ($1,200) and another charges 1.5% ($6,000), the first could save you thousands annually. However, you’ll need to weigh this against the lender’s other fees and the interest rate. Be prepared to pay for PMI when using our mortgage calculator for Florida also.

How to Lower Your Mortgage Payment in Florida

The average monthly payment in the state of Florida is around $1,400. But if you’re buying a home in Florida today, you’re likely to pay more. So, let’s talk about some ways you can lower your mortgage payment in Florida.

Find a Lower Interest Rate in Florida

Whether you’re using a mortgage calculator for Miami or Tallahassee, mortgage rates will play a big role in how much house you can afford. What you may not know is that lenders charge different rates depending on the area. This means it pays to shop around for interest rates.

Using our mortgage estimator for Florida, let’s say you got an offer for a 6.0% interest rate on a $400,000 loan. Assuming the average tax rate of 0.91% and $4,231 in property taxes, your monthly payment would be $3,084. Multiplying this by 360 loan payments over 30 years, you’d pay a total of $1,110,240. That means you’d pay $710,240 in interest, taxes, and insurance over the life of the loan.

Now say you get another offer for 5.5% interest. Your monthly payment would be $2,957. You’d pay $1,064,520 over 30 years. That’s $45,720 less due to 0.5% less interest. As you can see, finding a lower rate can help considerably. While it may not lower your monthly payment by a lot, over 30 years, that interest does add up.

Put Down More Money

Using our mortgage calculator for Florida, you can clearly see the effect of a larger down payment. It lowers your principal, so you’ll owe less, but there’s also less for your lender to charge interest on. If you put more money down, you may also qualify for a lower interest rate. Remember that lenders charge PMI on mortgages with less than 20% down. Avoiding PMI could lower your monthly payment by several hundred dollars.

Choose a Different Mortgage

You can always shop around for different lenders, but have you considered using a different mortgage type? A 30-year fixed-rate conventional mortgage is the industry standard, but you could find a lower rate with other options. Military veterans, for instance, can qualify for a lower rate with a VA loan.

Adjustable-rate mortgages (ARMs) offer a lower interest rate for a period, then adjust (often upward) every six months to a year. How much the rate changes after this period depends on the specifics of the loan. The good news is that this intro rate lasts 3 to 10 years. So you could sell the home or refinance before the low rate ends.

Buy a Cheaper House

This may seem obvious, but don’t underestimate the value of living within your means. If a house is too expensive for you, you’ll need to readjust your budget to accommodate it. The good news is that our mortgage calculator makes it easy for you. Once you plug in the numbers, it lets you see at a glance how much you’ll need to earn annually to afford the house.

Let’s work through an example of how this could help you. Start with the above scenario of a $400,000 mortgage at 5.5% interest. Plugging the Florida average property tax and insurance into the mortgage calculator for Florida, we get $2,957 monthly and $1,064,520 over 30 years of paying the loan.

Let’s say you decide to lower your budget by $25,000. You take out a $375,000 mortgage. Your monthly payment changes to $2,636, which is about $300 less each month. Over 30 years you’ll pay $948,960. That’s $115,560 less over 30 years. So, not only will you save the $25,000, but you’ll save all the interest on it, too.

Florida Housing Market

Florida is the third most populated state in the country behind California and Texas. It’s also one of the fastest-growing states, with over 18% growth since 2010. According to the real estate listing site RedFin, in February 2023 home prices in Florida grew by 4.8% year over year. The median selling price was $390,000. Currently, Monroe County is the most expensive county on average in the state.

However, this appears to be slowing as the number of homes sold was down by 24.8% year over year. On top of that, homes stayed on the market 49% longer.

So, while prices are currently high, there’s less competition than there was last year. There are also more homes on the market than this time last year, which could make sellers drop their prices if there’s not enough interest.

Interest rates are also up substantially vs. last year. This has an impact on relative affordability and is likely to drive prices down and slow the market.

Summary

For best results with our mortgage calculator for Florida, enter your specific insurance and tax information. The state has high demand for housing, with many people flocking there for the warm weather, beaches, and relaxed culture. Housing prices have risen in recent years, but are stabilizing and could decline in the future.

Do your research to find the best rate, shop in the area you want, and look into more accurate tax and insurance costs. The more specific the information you have, the better the estimate you’ll get from our mortgage calculator.

{kind=link}